import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

import warnings

warnings.filterwarnings("ignore")Ensemble Methods

An ensemble method is an approach that combines many simple “building ensemble block” models in order to obtain a single and potentially very powerful model.

We will now discuss bagging, random forests and boosting. These are ensemble methods for which the simple building block is a regression or a classification tree.

Bagging

The decision trees discussed suffer from high variance. On the other hand, averaging trees with relatively high variance will typically result in a low variance procedure, with the same or even lower bias (because we average).

Bootstrap Aggregation, or bagging, is a general-purpose procedure for reducing the variance of a statistical learning method; we introduce it here because it is particularly useful and frequently used in the context of decision trees.

Model Training

Bagging classifier and regressor are implemented by BaggingClassifier and BaggingRegressor classes from sklearn.ensemble module,respectively. Using base_estimator parameter, both BaggingClassifier and BaggingRegressor can take as input a user-specified base model along with its hyperparameters. Another important hyperparameter in these constructors is n_estimators (by default it is 10).

Recall that RandomForest bagging is simply a special case of a random forest with m = p. Therefore, the RandomForestClassifier() function can also be used to perform both bagging and random forests.

Bagging Classifier

Code

from sklearn.datasets import load_breast_cancer

cancer = load_breast_cancer()

df = pd.DataFrame(cancer.data, columns=cancer.feature_names)

# Add target

df['target'] = cancer.target

df.head(5)| mean radius | mean texture | mean perimeter | mean area | mean smoothness | mean compactness | mean concavity | mean concave points | mean symmetry | mean fractal dimension | ... | worst texture | worst perimeter | worst area | worst smoothness | worst compactness | worst concavity | worst concave points | worst symmetry | worst fractal dimension | target | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 17.99 | 10.38 | 122.80 | 1001.0 | 0.11840 | 0.27760 | 0.3001 | 0.14710 | 0.2419 | 0.07871 | ... | 17.33 | 184.60 | 2019.0 | 0.1622 | 0.6656 | 0.7119 | 0.2654 | 0.4601 | 0.11890 | 0 |

| 1 | 20.57 | 17.77 | 132.90 | 1326.0 | 0.08474 | 0.07864 | 0.0869 | 0.07017 | 0.1812 | 0.05667 | ... | 23.41 | 158.80 | 1956.0 | 0.1238 | 0.1866 | 0.2416 | 0.1860 | 0.2750 | 0.08902 | 0 |

| 2 | 19.69 | 21.25 | 130.00 | 1203.0 | 0.10960 | 0.15990 | 0.1974 | 0.12790 | 0.2069 | 0.05999 | ... | 25.53 | 152.50 | 1709.0 | 0.1444 | 0.4245 | 0.4504 | 0.2430 | 0.3613 | 0.08758 | 0 |

| 3 | 11.42 | 20.38 | 77.58 | 386.1 | 0.14250 | 0.28390 | 0.2414 | 0.10520 | 0.2597 | 0.09744 | ... | 26.50 | 98.87 | 567.7 | 0.2098 | 0.8663 | 0.6869 | 0.2575 | 0.6638 | 0.17300 | 0 |

| 4 | 20.29 | 14.34 | 135.10 | 1297.0 | 0.10030 | 0.13280 | 0.1980 | 0.10430 | 0.1809 | 0.05883 | ... | 16.67 | 152.20 | 1575.0 | 0.1374 | 0.2050 | 0.4000 | 0.1625 | 0.2364 | 0.07678 | 0 |

5 rows × 31 columns

The base estimator to fit on random subsets of the dataset. If None, then the base estimator is a DecisionTreeClassifier.

from sklearn.model_selection import train_test_split

from sklearn.preprocessing import StandardScaler

from sklearn.ensemble import BaggingClassifier as Bagging

from sklearn.tree import DecisionTreeClassifier

# Target vs Inputs

X = df.drop(columns=["target"]) # Covariates-Only

y = df["target"] # Target-Outcome

# Train vs Split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=0)

# Create the base classifier

base_classifier = DecisionTreeClassifier() # this is the default if we skip this step

# Number of base models (iterations)

n_estimators = 10 # default

# Initialize Bagging Classifier

bagging = Bagging(base_estimator=base_classifier, n_estimators=n_estimators, random_state=0)

# Train Model

bagging.fit(X_train, y_train)

# Predict

y_test_pred = bagging.predict(X_test)from sklearn.metrics import accuracy_score, mean_squared_error

print('Accuracy Train' , bagging.score(X_train, y_train).round(2) )

print('Accuracy Test' , bagging.score(X_test, y_test).round(2) )

print( 'Test MSE:', mean_squared_error(y_test, y_test_pred).round(2) )Accuracy Train 1.0

Accuracy Test 0.94

Test MSE: 0.06But maybe we can do better by using pruned trees:

Adjust base_estimator

import sklearn.model_selection as skm

from sklearn.tree import DecisionTreeClassifier

# Initialize Decision Tree Regressor

dtree = DecisionTreeClassifier(random_state=0)

ccp_path = dtree.cost_complexity_pruning_path(X_train, y_train)

kfold = skm.KFold(10, random_state=1, shuffle=True)

grid = skm.GridSearchCV(dtree,

{'ccp_alpha': ccp_path.ccp_alphas},

refit=True, cv=kfold, scoring='accuracy')

grid.fit(X_train, y_train)

print('Optimal Alpha:', grid.best_score_.round(2))Optimal Alpha: 0.93# Create the base classifier

base_classifier = grid.best_estimator_

# Number of base models (iterations)

n_estimators = 10

# Initialize Bagging Classifier

bagging = Bagging(base_estimator=base_classifier, n_estimators=n_estimators, random_state=0)

# Train Model

bagging.fit(X_train, y_train)

# Predict

y_test_pred = bagging.predict(X_test)from sklearn.metrics import accuracy_score, mean_squared_error

print('Accuracy Train' , bagging.score(X_train, y_train).round(2) )

print('Accuracy Test' , bagging.score(X_test, y_test).round(2) )

print( 'Test MSE:', mean_squared_error(y_test, y_test_pred).round(2) )Accuracy Train 0.97

Accuracy Test 0.96

Test MSE: 0.04It is better! And with less overfitting, but better test performance.

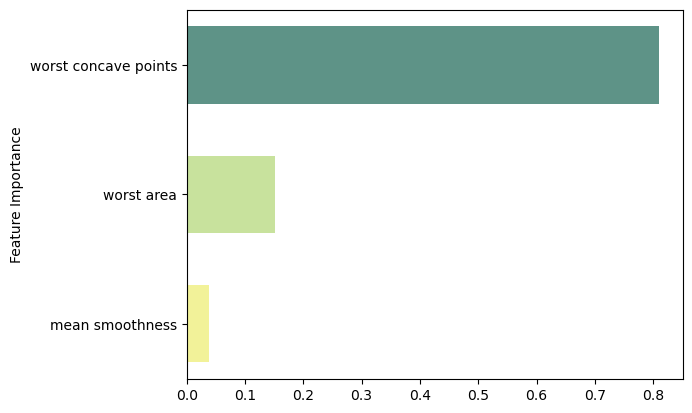

Feature Importance

Code

feat_importance = bagging.base_estimator_.feature_importances_

column_names = df.drop(columns='target').columns.tolist()

fimp_df = pd.DataFrame(feat_importance, column_names).reset_index().sort_values(0, ascending=False).head(3)

# Setup

fig, ax = plt.subplots()

# Setup

data = fimp_df.loc[:,0].sort_values()

index = np.arange(data.shape[0])

bar_labels = fimp_df.sort_values(0).loc[:,'index'].tolist()

bar_colors = ['#F2F299', '#C8E29D', '#5E9387', '#58828B']

bar_width = 0.6

# Figure

ax.barh(index, data, bar_width, label=bar_labels, color=bar_colors)

# Labels

ax.set_ylabel('Feature Importance')

ax.set_yticks(index, labels=bar_labels)

# Show

plt.show()

Bagging Regressor

Code

from ISLP import load_data, confusion_table

df = load_data("Boston")

df.head(5)| crim | zn | indus | chas | nox | rm | age | dis | rad | tax | ptratio | lstat | medv | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.00632 | 18.0 | 2.31 | 0 | 0.538 | 6.575 | 65.2 | 4.0900 | 1 | 296 | 15.3 | 4.98 | 24.0 |

| 1 | 0.02731 | 0.0 | 7.07 | 0 | 0.469 | 6.421 | 78.9 | 4.9671 | 2 | 242 | 17.8 | 9.14 | 21.6 |

| 2 | 0.02729 | 0.0 | 7.07 | 0 | 0.469 | 7.185 | 61.1 | 4.9671 | 2 | 242 | 17.8 | 4.03 | 34.7 |

| 3 | 0.03237 | 0.0 | 2.18 | 0 | 0.458 | 6.998 | 45.8 | 6.0622 | 3 | 222 | 18.7 | 2.94 | 33.4 |

| 4 | 0.06905 | 0.0 | 2.18 | 0 | 0.458 | 7.147 | 54.2 | 6.0622 | 3 | 222 | 18.7 | 5.33 | 36.2 |

from sklearn.model_selection import train_test_split

from sklearn.preprocessing import StandardScaler

from sklearn.ensemble import BaggingRegressor as Bagging

from sklearn.tree import DecisionTreeRegressor

# Target vs Inputs

X = df.drop(columns=["medv"]) # Covariates-Only

y = df["medv"] # Target-Outcome

# Train vs Split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=0)

# Create the base classifier

base_classifier = DecisionTreeRegressor() # this is the default if we skip this step

# Number of base models (iterations)

n_estimators = 10 # default

# Initialize Bagging Classifier

bagging = Bagging(base_estimator=base_classifier, n_estimators=n_estimators, random_state=0)

# Train Model

bagging.fit(X_train, y_train)

# Predict

y_test_pred = bagging.predict(X_test)from sklearn.metrics import accuracy_score, mean_squared_error

print('R2 Train' , bagging.score(X_train, y_train).round(2) )

print('R2 Test' , bagging.score(X_test, y_test).round(2) )

print( 'Test MSE:', mean_squared_error(y_test, y_test_pred).round(2) )R2 Train 0.98

R2 Test 0.74

Test MSE: 21.37Adjust base_estimator

import sklearn.model_selection as skm

from sklearn.tree import DecisionTreeRegressor

# Initialize Decision Tree Regressor

dtree = DecisionTreeRegressor(random_state=0)

ccp_path = dtree.cost_complexity_pruning_path(X_train, y_train)

kfold = skm.KFold(5, shuffle=True, random_state=10)

# Grid Search

grid = skm.GridSearchCV(dtree, {'ccp_alpha': ccp_path.ccp_alphas}, refit=True, cv=kfold, scoring='neg_mean_squared_error')

# Fit Model

G = grid.fit(X_train, y_train)

print('Optimal Alpha:', grid.best_score_.round(2))Optimal Alpha: -15.28# Create the base regressor

base_regressor = grid.best_estimator_

# Number of base models (iterations)

n_estimators = 10

# Initialize Bagging Regressor

bagging = Bagging(base_estimator=base_regressor, n_estimators=n_estimators, random_state=0)

# Train Model

bagging.fit(X_train, y_train)

# Predict

y_test_pred = bagging.predict(X_test)from sklearn.metrics import accuracy_score, mean_squared_error

print('R2 Train' , bagging.score(X_train, y_train).round(2) )

print('R2 Test' , bagging.score(X_test, y_test).round(2) )

print( 'Test MSE:', mean_squared_error(y_test, y_test_pred).round(2) )Accuracy Train 0.95

Accuracy Test 0.73

Test MSE: 21.7In this case, the pruned tree performance is slightly worse.

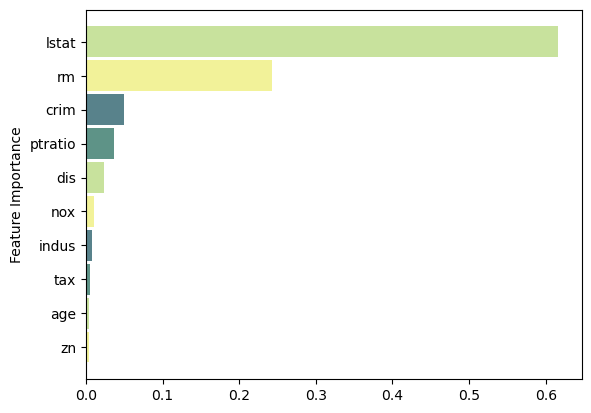

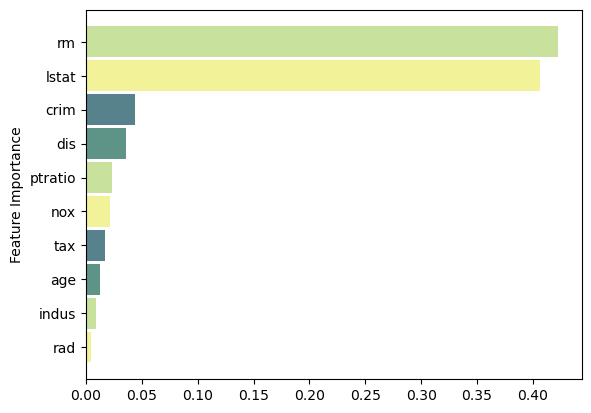

Feature Importance

Code

feat_importance = bagging.base_estimator_.feature_importances_

column_names = df.drop(columns='medv').columns.tolist()

fimp_df = pd.DataFrame(feat_importance, column_names).reset_index().sort_values(0, ascending=False).head(10)

# Setup

fig, ax = plt.subplots()

# Setup

data = fimp_df.loc[:,0].sort_values()

index = np.arange(data.shape[0])

bar_labels = fimp_df.sort_values(0).loc[:,'index'].tolist()

bar_colors = ['#F2F299', '#C8E29D', '#5E9387', '#58828B']

bar_width = 0.9

# Figure

ax.barh(index, data, bar_width, label=bar_labels, color=bar_colors)

# Labels

ax.set_ylabel('Feature Importance')

ax.set_yticks(index, labels=bar_labels)

# Show

plt.show()

Random Forest

With bagging we are using in each split the full set of \textbf X variables available, so we tend to construct very similar trees. Therefore, the trees will be very correlated, and their average will not result in a variance reduction. - If there is a strong predictor in the dataset, most or all trees will be similar to each other since the top split will be the strong predictor. Consequently, all of the bagged trees will look quite similar to each other.

In Random Forests, at each split, we take a random sample of m covariates chosen as split candidates from the full set of p predictors. A fresh sample of m predictors is taken at each split.

- The split is allowed to use only one of those m predictors.

- The default is m \approx \sqrt{p} for classification and m=p/3 for regression.

Decorrelating Trees: Random forests overcome this problem by forcing each split to consider only a subset of the predictors.

The main difference between bagging and random forests is the choice of predictor subset size m. For instance, if a random forest is built using m = p, then this amounts simply to bagging.

Model Training

The random forest classifier and regressor are implemented in RandomForestClassifier and RandomForestRegressor classes from sklearn.ensemble module, respectively. Many hyperparameters in these algorithms are similar to scikit-learn implementation of CART with the same functionality but applied to all underlying base trees.

Random Forest Classifier

Code

from sklearn.datasets import load_breast_cancer

from sklearn.model_selection import train_test_split

from sklearn.preprocessing import StandardScaler

# Breast Cancer Data

cancer = load_breast_cancer()

df = pd.DataFrame(cancer.data, columns=cancer.feature_names)

df['target'] = cancer.target

# Target vs Inputs

X = df.drop(columns=["target"]) # Covariates-Only

y = df["target"] # Target-Outcome

# Train vs Split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=0)from sklearn.ensemble import RandomForestClassifier as RF

# Initialize Random Forest Classifier

rforest = RF(random_state=0)

# Train Model

rforest.fit(X_train, y_train)

# Predict

y_test_pred = rforest.predict(X_test)from sklearn.metrics import accuracy_score, mean_squared_error

print('Accuracy Train' , rforest.score(X_train, y_train).round(2) )

print('Accuracy Test' , rforest.score(X_test, y_test).round(2) )

print( 'Test MSE:', mean_squared_error(y_test, y_test_pred).round(2) )Accuracy Train 1.0

Accuracy Test 0.96

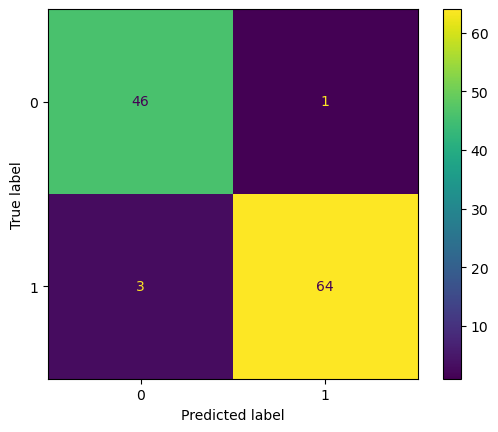

Test MSE: 0.04Code

import matplotlib.pyplot as plt

from sklearn.metrics import ConfusionMatrixDisplay

ConfusionMatrixDisplay.from_estimator(rforest, X_test, y_test)

plt.show()

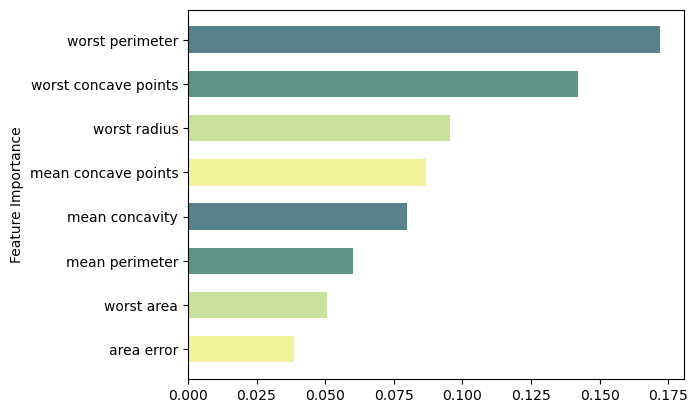

Feature Importance

Code

feat_importance = rforest.feature_importances_

column_names = df.drop(columns='target').columns.tolist()

fimp_df = pd.DataFrame(feat_importance, column_names).reset_index().sort_values(0, ascending=False).head(8)

# Setup

fig, ax = plt.subplots()

# Setup

data = fimp_df.loc[:,0].sort_values()

index = np.arange(data.shape[0])

bar_labels = fimp_df.sort_values(0).loc[:,'index'].tolist()

bar_colors = ['#F2F299', '#C8E29D', '#5E9387', '#58828B']

bar_width = 0.6

# Figure

ax.barh(index, data, bar_width, label=bar_labels, color=bar_colors)

# Labels

ax.set_ylabel('Feature Importance')

ax.set_yticks(index, labels=bar_labels)

# Show

plt.show()

Random Forest Regressor

Code

from ISLP import load_data, confusion_table

from sklearn.model_selection import train_test_split

from sklearn.preprocessing import StandardScaler

# Boston Dataset

df = load_data("Boston")

# Target vs Inputs

X = df.drop(columns=["medv"]) # Covariates-Only

y = df["medv"] # Target-Outcome

# Train vs Split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=0)from sklearn.ensemble import RandomForestRegressor as RF

# Initialize Random Forest Regressor

rforest = RF(random_state=0)

# Train Model

rforest.fit(X_train, y_train)

# Predict

y_test_pred = rforest.predict(X_test)from sklearn.metrics import accuracy_score, mean_squared_error

print('R2 Train' , rforest.score(X_train, y_train).round(2) )

print('R2 Test' , rforest.score(X_test, y_test).round(2) )

print( 'Test MSE:', mean_squared_error(y_test, y_test_pred).round(2) )R2 Train 0.98

R2 Test 0.77

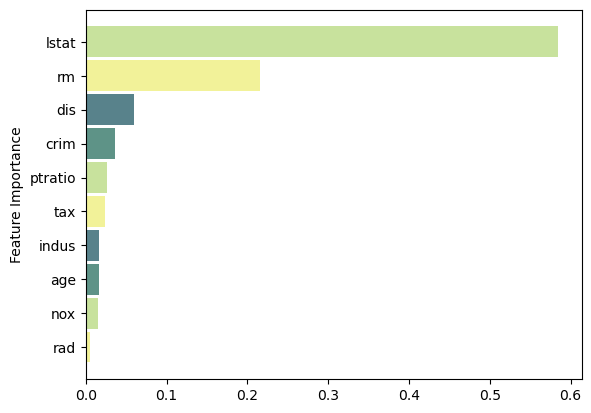

Test MSE: 18.71Feature Importance

Code

feat_importance = rforest.feature_importances_

column_names = df.drop(columns='medv').columns.tolist()

fimp_df = pd.DataFrame(feat_importance, column_names).reset_index().sort_values(0, ascending=False).head(10)

# Setup

fig, ax = plt.subplots()

# Setup

data = fimp_df.loc[:,0].sort_values()

index = np.arange(data.shape[0])

bar_labels = fimp_df.sort_values(0).loc[:,'index'].tolist()

bar_colors = ['#F2F299', '#C8E29D', '#5E9387', '#58828B']

bar_width = 0.9

# Figure

ax.barh(index, data, bar_width, label=bar_labels, color=bar_colors)

# Labels

ax.set_ylabel('Feature Importance')

ax.set_yticks(index, labels=bar_labels)

# Show

plt.show()

Boosting

In Bagging, each tree is built on a bootstrap data set, independent of the other trees. Boosting works in a similar way, except that the trees are grown sequentially: each tree is grown using information from previously grown trees.

Boosting does not involve bootstrap sampling; instead each tree is fit on a modified version of the original data set.

Unlike fitting a single large decision tree to the data, which amounts to fitting the data hard and potentially overfitting, the boosting approach instead learns slowly, building smaller trees. - Given the current model, we fit a decision tree to the residuals from the model. - Note that in boosting, unlike in bagging, the construction of each tree depends strongly on the trees that have already been grown.

Model Training

Here we will only use Regressor as example, but the same procedure applies for the Classifier methods.

Code

from ISLP import load_data, confusion_table

from sklearn.model_selection import train_test_split

from sklearn.preprocessing import StandardScaler

# Boston Dataset

df = load_data("Boston")

# Target vs Inputs

X = df.drop(columns=["medv"]) # Covariates-Only

y = df["medv"] # Target-Outcome

# Train vs Split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=0)AdaBoost

AdaBoost.SAMME can be implemented using AdaBoostClassifier from sklearn.ensemble module by setting the algorithm parameter to SAMME. AdaBoost.R2 is implemented by AdaBoostRegressor from the same module. Using base_estimator parameter, both AdaBoostClassifier and AdaBoostRegressor can take as input a user-specified base model along with its hyperparameters. - If this parameter is not specified, by default a decision stump (a DecisionTreeClassifier with max_depth of 1) will be used.

from sklearn.ensemble import AdaBoostRegressor as boosting

# Initialize Boosting Regressor

adaboost = boosting(random_state=0)

# Train Model

adaboost.fit(X_train, y_train)

# Predict

y_test_pred = adaboost.predict(X_test)from sklearn.metrics import accuracy_score, mean_squared_error

print('R2 Train' , adaboost.score(X_train, y_train).round(2) )

print('R2 Test' , adaboost.score(X_test, y_test).round(2) )

print( 'Test MSE:', mean_squared_error(y_test, y_test_pred).round(2) )R2 Train 0.92

R2 Test 0.64

Test MSE: 29.02Adjust base_estimator

import sklearn.model_selection as skm

from sklearn.tree import DecisionTreeRegressor

# Initialize Decision Tree Regressor

dtree = DecisionTreeRegressor(random_state=0)

ccp_path = dtree.cost_complexity_pruning_path(X_train, y_train)

kfold = skm.KFold(5, shuffle=True, random_state=10)

# Grid Search

grid = skm.GridSearchCV(dtree, {'ccp_alpha': ccp_path.ccp_alphas}, refit=True, cv=kfold, scoring='neg_mean_squared_error')

# Fit Model

G = grid.fit(X_train, y_train)

print('Optimal Alpha:', grid.best_score_.round(2))Optimal Alpha: -15.28# Create the base regressor

base_regressor = grid.best_estimator_

# Number of base models (iterations)

n_estimators = 50 # default

# Initialize Bagging Regressor

adaboost = boosting(base_estimator=base_regressor, n_estimators=n_estimators, random_state=0)

# Train Model

adaboost.fit(X_train, y_train)

# Predict

y_test_pred = adaboost.predict(X_test)from sklearn.metrics import accuracy_score, mean_squared_error

print('R2 Train' , adaboost.score(X_train, y_train).round(2) )

print('R2 Test' , adaboost.score(X_test, y_test).round(2) )

print( 'Test MSE:', mean_squared_error(y_test, y_test_pred).round(2) )R2 Train 0.98

R2 Test 0.67

Test MSE: 26.62Feature Importance

Code

feat_importance = adaboost.feature_importances_

column_names = df.drop(columns='medv').columns.tolist()

fimp_df = pd.DataFrame(feat_importance, column_names).reset_index().sort_values(0, ascending=False).head(10)

# Setup

fig, ax = plt.subplots()

# Setup

data = fimp_df.loc[:,0].sort_values()

index = np.arange(data.shape[0])

bar_labels = fimp_df.sort_values(0).loc[:,'index'].tolist()

bar_colors = ['#F2F299', '#C8E29D', '#5E9387', '#58828B']

bar_width = 0.9

# Figure

ax.barh(index, data, bar_width, label=bar_labels, color=bar_colors)

# Labels

ax.set_ylabel('Feature Importance')

ax.set_yticks(index, labels=bar_labels)

# Show

plt.show()

Gradient Boosting

GBRT for classification and regression are implemented using GradientBoostingClassifier and GradientBoostingRegressor classes from sklearn.ensemble module, respectively. By default a regression tree of max_depth of 3 will be used as the base learner. The n_estimators=100 parameter controls the maximum number of base models (M in the aforementioned algorithms). The supported loss values for GradientBoostingClassifier are deviance and exponential, and for GradientBoostingRegressor are squared_error, absolute_error, and two more options.

from sklearn.ensemble import GradientBoostingRegressor as boosting

# Initialize Boosting Regressor

gradient = boosting(random_state=0)

# Train Model

gradient.fit(X_train, y_train)

# Predict

y_test_pred = gradient.predict(X_test)from sklearn.metrics import accuracy_score, mean_squared_error

print('R2 Train' , gradient.score(X_train, y_train).round(2) )

print('R2 Test' , gradient.score(X_test, y_test).round(2) )

print( 'Test MSE:', mean_squared_error(y_test, y_test_pred).round(2) )R2 Train 0.98

R2 Test 0.78

Test MSE: 17.98XGBoost

XGBoost is not part of scikit-learn but its Python library can be installed and it has a scikit-learn API that makes it accessible similar to many other estimators in scikit-learn. One can use Conda package manager to install xgboost package for Python.

As XGBoost is essentially a form of GBRT, it can be used for both classification and regression.

- The classifier and regressor classes can be imported as from

xgboost import XGBClassifierand fromxgboost import XGBRegressor, respectively. - Once imported, they can be used similarly to scikit-learn estimators. Some of the important hyperparameters in these classes are

n_estimators,max_depth,gamma,reg_lambda, andlearning_rate.

from xgboost import XGBRegressor as boosting

# Initialize Boosting Regressor

xgb = boosting(random_state=0)

# Train Model

xgb.fit(X_train, y_train)

# Predict

y_test_pred = xgb.predict(X_test)from sklearn.metrics import accuracy_score, mean_squared_error

print('R2 Train' , xgb.score(X_train, y_train).round(2) )

print('R2 Test' , xgb.score(X_test, y_test).round(2) )

print( 'Test MSE:', mean_squared_error(y_test, y_test_pred).round(2) )R2 Train 1.0

R2 Test 0.73

Test MSE: 22.39